This is the first in a multi-part series titled “Trust, Not Transactions” where we separate hype from reality in a number of aspects of blockchain, both operational and technological.

Much of the focus of the discussions surrounding blockchain, and especially cryptocurrencies, has centered around centralization versus decentralization.

The simplified discussion usually points Bitcoin (or other cryptocurrencies) as being globally decentralized and permissionless, and any system in the financial sector as being centralized and closed.

As with any good oversimplification, this is superficially correct but at the same time, misses the point entirely.

When you take a look behind the curtain, it becomes quite obvious that both views are based in a utopian mindset, where everything slots into perfect definitions. In reality, Bitcoin is much more centralized, fragile, and permissioned than general perception, while the finance industry is much less centralized and monolithic than generally given credit for.

This disconnect comes from a combination of misunderstanding where the value comes from in financial services while also viewing architectural and business decisions through an ideological lens.

Not only does this lead to a disconnect between the reality of the current situation, but it leads to developing product and infrastructure roadmaps that don’t fundamentally address market needs.

It also glosses over constructs that don’t fit neatly into either category, such as Federated Blockchain networks, which we introduce in more detail below.

While the following grossly oversimplifies the moving parts in the system, what the Financial Industry in general is trying to accomplish in most functions generally boils down to moving and tracking two counterparties.

In effect, this boils down to creating a tradeable receipt that an authorized party (eg, Central Bank, company director, derivatives trader) made a statement that they were issuing a security (or contract), and the identity of the party to whom they initially issued it.

While this is a bit abstract, this is in effect what a share in a company, or collateral issued in a derivatives contract is: assurance that you hold a claim on the issuing party and the ability to transfer that claim to others.

At the same time, financial services providers need to comply with relatively complex regulations that may be vastly different across jurisdictions.

Taking that view of what need we are trying to fill, we can better understand how the mechanics and incentives of centralized or decentralized networks contribute to filling that need.

Decentralization vs Centralization

Centralized Networks

In this (simplified) model, a centralized service is effectively a black box that users engage directly in a one-to-one relationship.

In this model, the party validating transactions, the party recording transaction history, and the party holding custody of value are all the same.

In reality, this service generally then interacts with another centralized service that coordinates this custodianship so value can be transacted between two or more end users that use different custodians. This allows for fungibility of assets across different services without those services needing to trust each other.

This mechanism is also generally used for the initial dematerialization of assets and cash.

At an ecosystem level this manifests as a global hub-and-spoke model. Under this model, actions taken by end users being reflected in a shared settlement ledger at some point in the future several organizations below the retail service provider.

Decentralized Networks

Conversely, a decentralized network relies on a network of validators that ensure the rules of the service are followed by all users, and users can engage any of the validators (either directly or through another peer) to interact with the service.

As a result, the validators collectively effectively act as a service provider.

Cryptocurrencies like Bitcoin mostly transact in a native token although protocols have been built on top of most cryptocurrencies to allow custodians to issue held value to addresses.

With this construct, the blockchain network takes on the role of the clearing & settlement, allowing the issued token to be redeemable against the custodian who issued the tokenized asset.

If two or more custodians trusted each other or were able to dematerialize their securities to the blockchain directly, fungibility between custodians could be directly established as well, much like it is in the hub-and-spoke model.

Benefits & Tradeoffs

As we can see, each of these approaches comes with it’s own set of strengths and weaknesses:

Benefits of a Hub-and-Spoke Approach

- Technical efficiency

- Easier to meet regulatory compliance

Disadvantages of a Hub-and-Spoke Approach

- Process and labor inefficient

- Inability to change infrastructure once installed without massive cost and time investment.

Benefits of a Decentralized Approach

- No single point of political censorship or failure

Disadvantages of a Decentralized Approach

- Technologically inefficient

- Inability to change infrastructure once installed without massive cost and time investment.

- Potential inability to meet regulatory compliance

The benefits from either approach both come from everyone agreeing on the same source of collective truth about what assets exist and who owns them.

Unfortunately, that means if we hold value in separate networks in either system, we need central parties that allow us to transfer or trade assets across different networks while taking on counterparty risk.

In each approach, we also see that the need for a global consensus on what specific ledger/database holds the “golden record” for what assets are issued and who owns them, presents a massive coordination problem.

In order to make changes to the underlying value transfer, overwhelming consensus is necessary under either approach. Then once (if) consensus is achieved, it can be a brittle, long, and expensive rollout process that requires 100% of participants to upgrade before migration.

It will often be easier and cheaper to build a new, incompatible network that allows for the desired improvements than changing the existing structure. Otherwise, innovation is left to layers closer to the end user, as we have seen with the proliferation of mobile payment apps in the past few years.

Thankfully, we have a construct that avoids this.

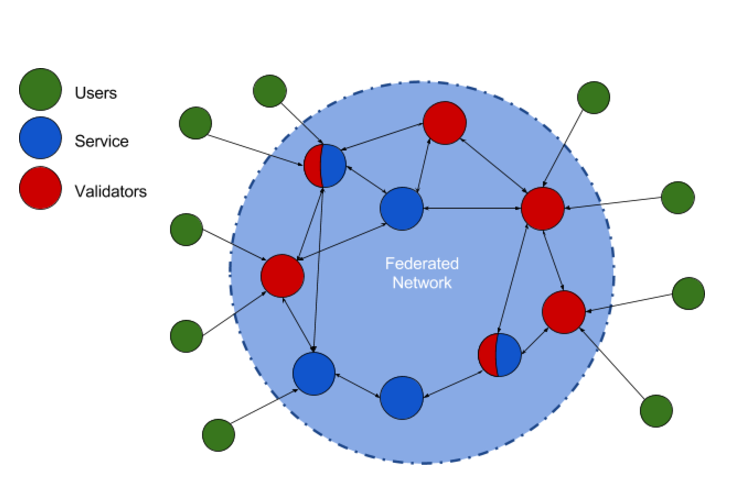

The Federated Alternative

One of the great things about new technology is that you often have a chance to step outside the established mindset and try something new.

One of the conclusions we have come to at Credits when researching how we might address the issue of custodians and settlement is that federated blockchain networks offer much of the best of both worlds.

Building a Federated Network

Our view of a federated blockchain network starts off looking a lot like a decentralized blockchain where custodians can issue value (albeit one not reliant on Proof of Work and that allows for RBAC).

In a federated network, you still have multiple parties acting as gatekeeper, maintaining and adding to the history of the ledger; collectively making it immutable after each confirmed block.

In some networks, validators may also be service providers and/or value issuers, but the two roles are fundamentally able to be separated from each other.

Federated Network of Federated Networks

Building on that, we can start connecting separate federated networks together, allowing value and information to be issued and utilized across network boundaries.

Cryptographic proofs that value has been issued can then be transported across different networks that know how to communicate with each other, allowing for the instant and atomic transport of value across networks.

This is allowed due to the way these assets are issued as cryptographic tokens and is similar to the concepts presented in Sidechains4, but using consensus methods that allow for faster (and truly atomic) validity across networks5.

Transactions can even be processed that involve multiple parties across multiple networks that happen atomically across networks without requiring a central party to act as arbiter and hold counterparty risk.

Assuming that the provenance of the initial issuance can be linked back to the currently held asset, it doesn’t matter which network it lives in, the “tokenized” asset acts as a receipt on the initial issuer whether that asset is cash, equity, property, or contract.

This allows us to overcome the huge inertia problem that plagues both decentralized and hub-and-spoke networks by having the asset truly live in the protocol, rather than be tied to a particular network’s implementation and the users & validators who participate in it.

As we move toward real problems being solved using blockchain technology, this focus on provenance of value is going to increasingly guide technology choices when building new financial technology.

If successful, this will decouple the implementation for accessing and transferring value from the protocol that allows any network to hold custody of value, removing barriers to changing providers or jurisdictions, increasing liquidity, and lowering costs.

Conclusion

The oversimplification of decentralization vs centralization is one of many false dichotomies the fledgling blockchain industry is working through at the moment.

This oversimplification leads to the championing of solutions that don’t solve anyone’s actual problems and the demonization of existing solutions due to not understanding why they were built in the first place6.

Instead, if we deconstruct the actual moving parts of the problem we’re looking to address, this allows us to work backward from the priorities of the use case and pick the tools and constructs that best address the need.

In this case, that led us to the solution of interoperable, federated blockchains. This allows us to achieve the immutability, auditability, and process efficiency of the blockchain with the regulatory compliance and scalability of more centralized systems.

Allowing value issued on these networks to move from network to network then solves the problem of coordination and upgrade consensus, which is the most expensive and slowest part of the process for both centralized and decentralized solutions.

In the long run, this can allow us to decouple what counts as proof of issuance and ownership from the specific network we use to transfer and track value.

This path will help bring about an actual protocol of value to the internet, and this approach to blockchain infrastructure will make sure we don’t let the search for utopia prevent us from making an impact in the real world.

End Notes

1 - Bitcoin Centralization

- At the time of this post, the top 2 mining pools control 51% of the hashing power.

- Top 3 control 66%

- Top 4 control 80%

- Top 6 control 90%

- Bitfury’s new datacenter can bring about a 51% attack on its own once they finish bringing it online, regardless of the number mining pools they point their miners at.

- 5 developers must unanimously agree to any changes to Bitcoin Core, 3 of whom are employed by Blockstream.

- 1 person controls three of the most popular and longstanding Bitcoin websites.

2 - Financial Services Centralization

- While most financial services involve the movement of value that is either issued or tracked centrally in a given jurisdiction, customer-facing services are largely separate and competing, tying back into those central services in a hub-and-spoke model.

- These central issuers/custodians often came about as a result of financial institutes wanting to be able to work together but not being able to fully trust each other, thus needing some mechanism serving as a neutral ground for verifying and recording transactions between themselves, often on a netting basis through a Clearing House, or similar mechanism.

- That is, the Lightning Network, but 225 years old.

3 - Ignoring Problems with Approach

This has led to two major distractions during 2015:

- The Bitcoin community has stuck its head in the ground regarding the actual state & momentum of the cryptocurrency ecosystem and whether or not they’re providing real value.

- Parts of the financial services industry still initially view use cases of blockchain technology through the lense of cryptocurrency, making the benefit vs trade-off conversation longer and more convoluted.

4 - Sidechains

- Richard Gendal Brown explaining Sidechains - http://gendal.me/2014/10/26/a-simple-explanation-of-bitcoin-sidechains/

- Peter Todd’s Security Concerns - https://www.reddit.com/r/Bitcoin/comments/2k01du/peter_todd_on_twitter_the_sidechains_paper_is/clgpjpx

5 - Finality on Federated Crosschain Transactions

Crosschain transfers on Proof of Work based cryptocurrencies is problematic for two reasons:

- Merge-mined Sidechains allow for miners to steal funds transferred to those Sidechains.

- Finality is never fully achieved, confirmations only probabilistically approach finality assuming >51% of hashing power is honest.

- Under current ecosystem, this is likely irrelevant, but both the issuing of assets on top of PoW blockchains and introducing merge-mined sidechains substantially increase the incentives to re-order blockchain history.

- This is made slightly harder to do (surreptitiously at least) by waiting “a day or two” before allowing transferred funds to be used.

Other consensus mechanisms that don’t allow for reordering of history (leaderless Proof of Stake) solve the finality issue.

Ensuring the validators of the different networks are properly incentivized (whether directly financially, posted surety bond, liability, or regulation) additionally solves the issue of federated parties stealing funds issued on another network. Existing constructs for custody of funds in regulated environments should be sufficient.

6 - This Exists for no Reason

“In the matter of reforming things, as distinct from deforming them, there is one plain and simple principle; a principle which will probably be called a paradox. There exists in such a case a certain institution or law; let us say, for the sake of simplicity, a fence or gate erected across a road. The more modern type of reformer goes gaily up to it and says, “I don’t see the use of this; let us clear it away.” To which the more intelligent type of reformer will do well to answer: “If you don’t see the use of it, I certainly won’t let you clear it away. Go away and think. Then, when you can come back and tell me that you do see the use of it, I may allow you to destroy it.”